As January comes around, many in the marketing world eagerly await the annual review of the previous year and expectations for the new one produced by Bruce Biegel (pictured left) of the Winterberry Group. This is a magisterial ‘big picture’ look at the world of data-driven marketing performance and trends. CMOs and CFOs often use it to justify or explain both their budget process and early performance indicators.

No less valuable, but perhaps closer to the digital coalface, is the survey carried out by the Marketo team within their Marketing Nation community. It reviews what responders think about the challenges they expect to face this year. Steve Lucas of Marketo (pictured right) offers practical suggestions alongside the survey results.

Both are worth looking at in detail, and you will find them here (log in is free to view the full Winterberry report) and here. However, I am going to briefly summarise them and then pull together some common strands with thoughts of my own.

Comparing marketing predictions

This comparison should tell us whether marketing practitioners are equipped and resourced to deal with the major challenges ahead.

Let’s look first at the Winterberry Group. Bruce uses an impressive array of sources of both quantified (mostly US numbers) and qualitative research. This is what he says happened in 2017 (numbers are US unless otherwise stated):

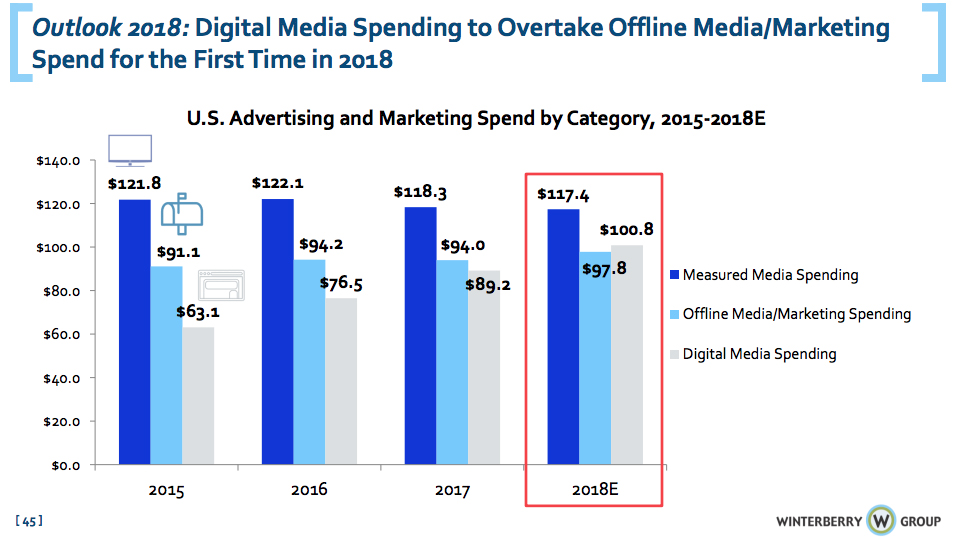

- Marketing spend slightly outpaced GDP growth – 2.9% vs. 2.7%

- Offline spend was flat – despite an unexpected 4.3% decline in direct mail spend

- Digital display overtook search for the first time in both dollars and growth percentage

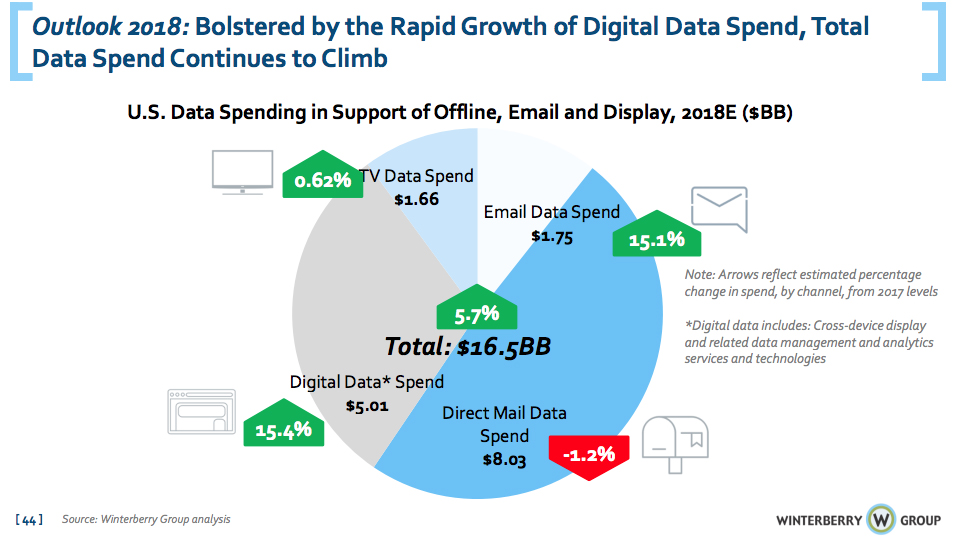

- Data spend outpaced ad spend growth, with digital data (which includes cross-device display and related data management and analytics) increasing 25.4% and email growing 15.1%. Offline data spend, perhaps reflecting direct mail decline, dropped 4.4% but in total dollars was still more than digital and email combined.

- On the mergers and acquisitions front, agency holding companies and consultancies focused heavily on digital agencies and martech providers – no surprise there.

- And the rise of the consultancies continued – organisations with a management consultancy heritage now occupy four of the top ten global agency slots

And the expectations for 2018?

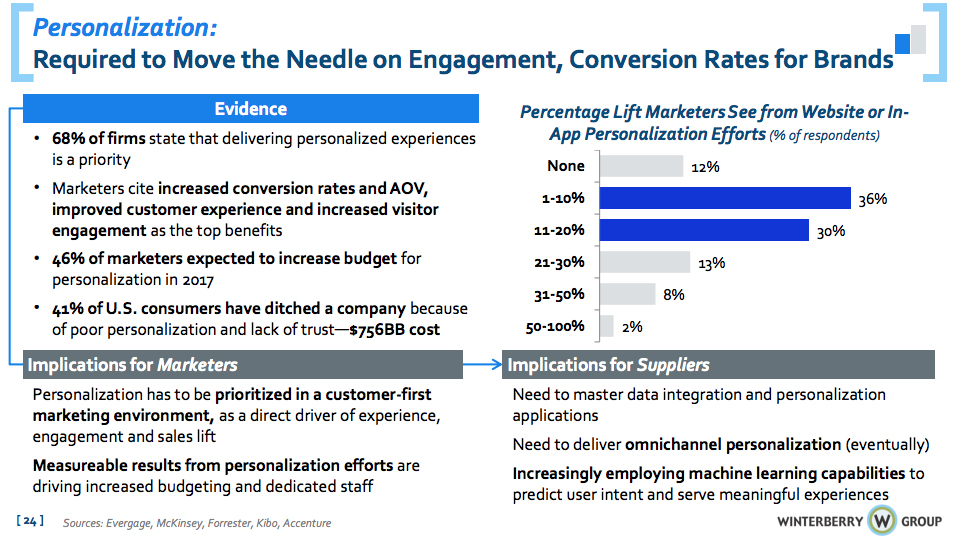

Bruce Biegel believes that email has been slow to integrate with the omni-channel world. Therefore, dynamic targeting, identity management (matching inbound responses with the database to facilitate relevant outbound communication), customer journey mapping and personalisation should be key goals for this year.

The research that he has gathered from multiple surveys from McKinsey, Accenture, Forrester and others indicate that 68% of marketers list personalisation as a priority, and 46% are putting money where their mouth is and allocating budget accordingly.

There is plenty more in the Winterberry guide – including forecasts for growth by media channel, e-commerce and loyalty trends, and the outlook for agencies, consultancies and adtech/martech. But let’s now look at what Marketo’s survey looks like.

Firstly, the good news. The questions posed by Marketo align pretty well with the landscape outlined by Winterberry. So, the analysts and experts are on the same page! Secondly, 50% of respondents said that their budgets were increasing this year. The money is going on, yes, personalised content, technology, account-based marketing (the survey will be skewed towards B2B) and analytics.

So far, so good. But the rest of the survey indicates both the distance that most marketers will have to travel to really tackle the main issues, and also how day-to-day issues and concerns are likely to be internal rather than external.

Marketo asked what percentage of content was personalised. Only 1% said all of it, 19% said most, 70% said some and 11% said none of it. But at least it seems that marketers know this is a goal that needs to be addressed.

I would have expected more progress – or at least responses that pretended that was the case – from the next question, which asked whether marketing activities tracked the buyers’ journey. Only 4% said very well, 33% said pretty well, 44% said OK and 19% said not well. And remember, the survey was carried out with Marketo’s community – so you would expect a high degree of familiarity with the potential of a marketing automation platform.

Only 20% say that they use artificial intelligence tools at the moment – although it is on the radar for almost all.

Marketo’s final question was: “Which activity will have the biggest impact on your business in 2018?” Here are the responses:

- Better sales and marketing alignment—24%

- Improved ability to track ROI—28%

- More comprehensive analytics—6%

- Better integration within my martech stack—13%

- Leveraging innovative marketing practices—10%

- Driving more value from my marketing spend—6%

- Working more closely with IT—1%

- Aligning my marketing activities to corporate business objectives—12%

This result indicates, at least to me, more of an eye towards internal meetings and reports rather than a vision for marketing excellence. Martech integration, analytics and innovation score low – and they would all be drivers of effective personalisation, identity management and the other trends and aspirations outlined in Winterberry.

The diminished focus on IT is, well, interesting.

Here are some conclusions:

- Tracking ROI – and presumably ROMI – is not an end in itself. The goal of marketing should be to maximise profitable revenue. If your ROMI is too high you are not being innovative enough and investing and testing too little.

- Achieving “better sales and marketing alignment” has to be measured by providing sales with the leads they need. It should have hard metrics not soft ones.

- CMOs have a responsibility to ensure that their marketing vision becomes part of their teams’ culture and embedded in execution models. That would be a real goal for 2018.

Have an opinion on this article? Please join in the discussion: the GMA is a community of data driven marketers and YOUR opinion counts.